Louisville is a city with character — and a lot of that character lives in its housing. From the grand Victorian homes of Old Louisville to the cozy bungalows of Germantown and the brick Craftsmans of the Highlands, this city’s older neighborhoods are part of what makes it such a wonderful place to live. But if you own or are thinking about buying one of these charming older homes, there are important factors you need to understand when insuring an older home.

At Aspen Ridge Insurance, we work with homeowners every day, and know which questions to ask to get the best coverage for you. Here’s what you should know.

Why Older Homes Are Harder (and More Expensive) to Insure

Age matters when insuring an older home — and not in a good way. According to data from MoneyGeek, older homes in Kentucky cost an average of $3,478 per year to insure, compared to just $2,222 for newer homes — a difference of over $1,250 annually. That’s a 56% premium increase simply due to the age of a property.

With a home build before 1940, you will want to consider if you would like to use vintage materials (such as plaster for the walls and ceilings), standard or modern materials (drywall for the walls and ceilings) or a combination. This will greatly change the cost to rebuild your home in the event of a large loss.

Why such a gap? Aging homes present greater risks across multiple systems: electrical, plumbing, roofing, and structural. Each of these can independently trigger higher premiums, reduced coverage, or even outright denial from a standard carrier.

The Big Four: Where Older Homes Commonly Run Into Trouble with Insurance

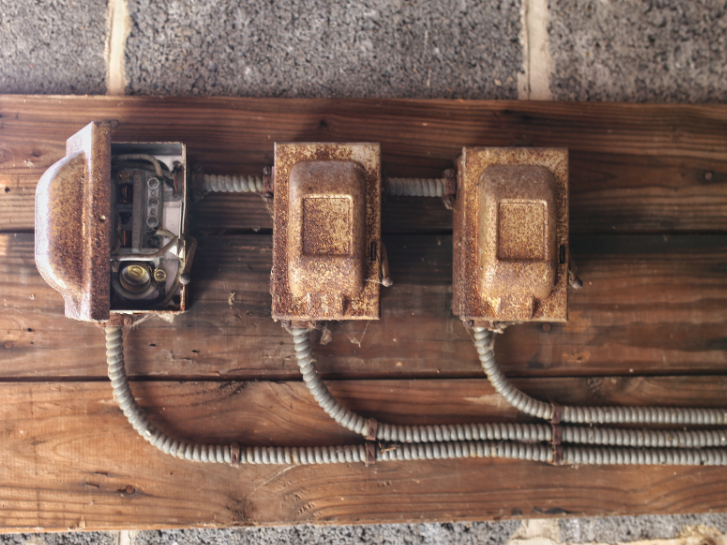

1. Electrical Systems

This is one of the most significant red flags for insurers when looking at older homes. Many Louisville homes built before the 1950s still have knob-and-tube wiring. This is an early electrical method using porcelain knobs and ceramic tubes. According to Insure.com, knob-and-tube wiring is considered such a serious fire hazard that many insurance companies simply won’t cover a home that still has it. The wiring lacks a ground wire, the rubber insulation deteriorates over time, and it can be easily overloaded by modern appliances and electronics.

Homes from the 1960s and 70s may have a different problem: aluminum wiring, which expands and contracts with heat and is prone to damage that can leave wires exposed — another significant fire risk.

If your older Louisville home still has one of these systems, expect your insurer to require an upgrade before they’ll write a policy — or charge substantially higher premiums if they’ll cover it at all.

2. Plumbing

Older plumbing materials are a major liability concern. Homes built before the 1960s often contain galvanized steel or lead pipes that corrode over time, leading to leaks and water damage. Many insurers require homeowners to update these systems with copper or PEX piping before they’ll offer full coverage. Beyond the insurance implications, aging pipes can quietly cause serious damage long before a leak becomes obvious.

3. Roofing

Roof age and material are among the first things an underwriter looks at. Older roofs, particularly those made from wood shake, slate, or tile, may not meet current safety standards and can be significantly more expensive to repair. If your roof is more than 20 years old, some insurers will only offer actual cash value coverage rather than replacement cost coverage, meaning depreciation will be deducted from your claim payout. A roof in poor condition can also result in outright denial.

At Aspen Ridge, we will look at both actual cash value and replacement cost, as well as different deductibles, to meet your individual needs as a home owner.

4. Building Codes and Ordinance Coverage

Here’s one that surprises many Louisville homeowners: when you file a claim on an older home, your contractor may be required to bring the damaged portion of the home up to current building codes — not the standards that existed when your home was built. This can significantly increase the cost of repairs. Standard policies often don’t cover this gap, which is why Ordinance or Law coverage is an important endorsement to consider for any older home.

Louisville’s Weather Adds Another Layer

Older homes in Louisville aren’t just dealing with wear and time — they’re also facing Kentucky’s active weather patterns. The state is prone to tornadoes, severe storms, and flooding, particularly near the Ohio River and its tributaries. Standard home insurance policies do not cover flood damage, which means Louisville homeowners in flood-prone areas need to secure a separate flood insurance policy through the National Flood Insurance Program (NFIP) or a private insurer.

If your home has already weathered decades of Kentucky weather, it’s worth having an inspector assess how well the structure, foundation, and roof have held up — both for your own knowledge and because an insurer may require an inspection before binding coverage.

What You Can Do to Improve Your Insurability

The good news: there are concrete steps you can take to make your older Louisville home more insurable and potentially reduce your premiums.

- Update the electrical system. Replacing knob-and-tube or aluminum wiring with modern wiring is often the single most impactful step you can take.

- Upgrade plumbing. Replacing galvanized steel or lead pipes with copper or PEX is both a safety improvement and an insurance one.

- Replace or reinforce the roof. A new roof — especially one with impact-resistant materials — can dramatically improve your coverage options and potentially earn you a discount.

- Install safety devices. Smoke detectors, CO alarms, a security system, and water leak sensors are all things insurers look favorably upon.

- Ask about Ordinance or Law coverage. Make sure your policy includes this endorsement so you’re not caught short if a claim triggers a required code upgrade.

- Work with an independent agent. Not all insurers treat older homes the same way. At Aspen Ridge Insurance, we can shop your risk across multiple carriers to find the best fit.

The Bottom Line

Owning an older home in Louisville means owning a piece of the city’s history — but it also means taking on a more complex insurance picture. Understanding the specific risks associated with your home’s age, systems, and construction type is the first step toward making sure you’re adequately protected.

At Aspen Ridge Insurance, we specialize in helping Louisville homeowners navigate exactly these kinds of situations. Whether you’re dealing with a century-old Victorian, a mid-century Craftsman, or anything in between, we’ll help you find coverage that actually fits your home.

Contact us today for a personalized review of your older home’s coverage needs.